We all know that saving money is important, and asking yourself “how much money should I save?” can be a difficult question to answer when beginning. Being a personal finance expert, I am asked this question a lot.

Between saving for emergencies, retirement, vacations, etc. there are a lot of things to consider. And, knowing how much to save is something that many people don’t often talk about. When it does come up, it can seem like there is no straight answer.

I’ve talked a lot about savings on this blog, and in my post 56% Of Americans Have Less Than $10,000 Saved For Retirement, I stated that 56% of Americans have less than an average of $10,000 in retirement savings and 33% have no retirement savings at all. This is something incredibly important to address!

Other interesting statistics mentioned in this article include:

- 42% of millennials have not begun saving for retirement.

- 52% of Gen Xers have less than $10,000 in retirement savings.

- About 30% of respondents age 55 and over have no retirement savings whatsoever.

- Nearly 75% of Americans over 40 are behind on saving for retirement.

There are many reasons for why a person may not save money each month, which I discuss further in the article.

However, one of the biggest reasons I’ve noticed is that people don’t realize that they should be saving more – because they think they’re “invincible” (they think they don’t need to save at the moment, they think they’ll never leave their job, etc), because they truly do think that they are saving enough money, or because they are so overwhelmed by the idea of saving money that they just don’t save any money at all.

Really, all of these reasons get back to the question I began with, “how much money should I save?” If you find that you are asking that question and not getting any straight answers, I am here to help you figure that out today.

Note: If you want to get serious about saving more money, I recommend trying Empower. It’s a free financial dashboard that lets you track your net worth, spending, and investments all in one place. Seeing your full financial picture can make it much easier to stay motivated and reach your savings goals.

Articles related to “how much money should I save?”:

- How To Save Money – My Best Money Saving Tips

- How I Retired In My 30s – From Ugly Crying To Retiring Just 10 Years Later

- How To Get Rich: The Steps To Build Wealth Now

- This 28 Year Old Retired With $2.25 Million

- How To Save For Retirement

So, how much money should I save each month?

According to the U.S. Bureau of Economic Analysis, the personal savings rate has averaged around 5% in the past year, and averaged 8.33% from 1959 until 2016.

There are a lot of people that think saving between 1% and 5% of their income is enough to be on track for retirement.

Sadly, it’s unlikely that amount will be enough to retire.

While 5% is better than nothing, just one small emergency each year could easily and completely wipe out that savings.

Further, saving just 5% means it will take you a very long time to retire.

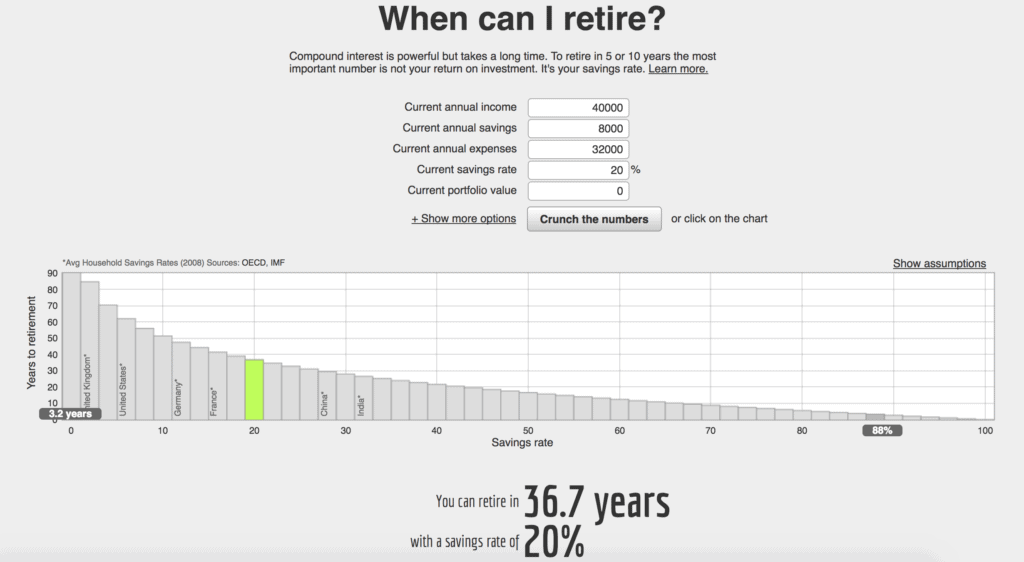

As you can see from the above:

- With just a 1% savings rate, it would take you 98.9 working years until you reach retirement.

- A 5% savings rate means that it would take you 66 working years to retire.

- A 20% savings rate means that it would take you 37 working years to retire.

- A 50% savings rate means that it would take you 17 working years to retire.

- A 75% savings rate means that it would take you 7 working years to retire.

So, by saving more of your money, you are likely to retire sooner. Makes sense, right?

Related content: Do You Know Your Net Worth?

Now, all of those statistics are dependant on how much you make, but for the average person, I recommend saving at least 20% of your income. That would still be around 37 years of working.

However, there is no perfect percentage.

If you have a high income, then you should probably save more of your income so that you aren’t just wastefully spending your money. For example, we save over 80% of our income each month after personal and business expenses.

On the other hand, if 20% just seems like a crazy high percentage for you to save, then just start somewhere, anywhere! Saving something is better than saving nothing (please head to the section below “Still think you can’t any save money?” for more information).

And, everyone has different financial goals. If you want to retire early, then you’ll most likely have to save more than 20% of your income.

Recommended reading: The 6 Steps To Take To Invest Your First Dollar – Yes, It’s Really This Easy!

Think about your goals when understanding “How much money should I save?”

One person’s answer to “how much money should I save?” will most likely be completely different from the next.

Due to that, your savings percentage goal can vary depending on your specific goals. Retirement calculators can be great and all, but you really need to make sure you are thinking about your own goals.

Remember though, it’s not always just about retirement. There are other things in your life that you may want to save for.

When asking yourself “how much money should I save?” you will want to think about your:

- Short-term goals – What are you saving for that you may purchase in the next year? This could be a vacation, an event you want to attend, holiday gifts, etc.

- Mid-term goals – Think of a goal that you want to reach in the next decade. This may include saving for a down payment on a house, buying a car, building up an emergency fund, etc.

- Long-term goals -This will most likely be your retirement goal, paying off your mortgage completely, etc.

Yes, that’s a lot to think about. And, this is why I always recommend saving as much as you realistically can.

Pay yourself first.

To make reaching your savings goals easier, I recommend starting to pay yourself first.

If you are unfamiliar with the idea, it’s basically setting aside money in savings before you pay any other bills. I also know someone who pays themselves first by putting extra money towards their debt before paying any other bills.

Paying yourself first before you pay your monthly expenses may be a scary thought. No one wants to over withdraw from their checking account or be unable to pay their monthly bills.

However, your future is just as important too, so it is much better to think about saving money as a need instead of something that can be pushed aside. Or, you can look at it this way, saving money is a bill you pay to yourself.

Paying yourself first becomes the first thing you do with each paycheck – you don’t even pay your other bills first. When you turn savings into a budget line item, rather than just putting what’s leftover into savings, it really can help you save more money. Yes, it may be difficult at first, but you will get used to living on less money.

For this to become part of your answer to the question “how much money should I save?” you may have to do some cutbacks with your budget or find ways to make more money. But, by only having a limited amount of money to spend each month, you will find that you are more closely watching your spending.

This may allow you to really see what is a need and what is just a want.

Here are my tips so that you can pay yourself first:

- Take a look at how much you are currently saving and spending each month. Start tracking your spending a little more closely and see how much of that is actually unneeded. Calculate how much money you should be saving each month and set that aside at the beginning of each month.

- Make it automatic. To make it easier and to simplify your finances, you may want to autopay a certain amount of money for savings each month.

- If you feel uncomfortable with paying yourself first, then you may want to find ways to cut your budget back or make more money.

Still think you can’t save any money?

Okay, so now you may be thinking “How much money should I save, if I don’t have much money?!”

Thinking about that recommended 20% savings number can be frustrating if you are already having a hard time paying your bills and/or living paycheck to paycheck.

However, I recommend saving as much money as you realistically can. This may be nowhere near 20% at first, heck, this might not even be 5%, but any little bit will help. If you are not able to save that much, just save something! Start with $25 a month if you have to – seriously, every little bit does help.

Even if it’s just $1 a day, set that amount aside and start saving it.

So, no matter how you are doing right now, just start with something, no matter how small. Then, work your way up until you are saving a percentage of your income that you are happy with.

Start small and work your way towards your savings goal. And, if you are currently paying off debt, keep in mind that it counts too! Just keep moving in a positive direction and keep getting closer and closer to reaching your financial goals.

Remember that 5% of your income most likely won’t be enough for the average person to retire, so you will want to continue to improve that percentage well into the future so that you will be able to retire one day.

I understand that some people have financial situations in which they may not be able to save as much money as they would like. Living paycheck to paycheck, being in medical debt, or having a major unexpected expense can wreck a person’s financial situation and their goals, and I understand that.

However, you will need to find a way out of that. To find a way out, you may want to find ways to cut your spending, make more money (learn ways to make extra money), and more. You will have to challenge yourself, and it may not be easy. However, it will all be worth it once you reach your financial goals!

By spending less money, you’ll decrease the amount of money you need for the future, including money for emergency funds, retirement, and more.

Just think about it: If you are currently living a frugal lifestyle, then you will be used to living on less in the future. This means that your saved retirement amount doesn’t need to be as large, which means it may be easier to reach that savings goal.

Also, if you start saving now, you can take advantage of compound interest, which I’ll talk about next.

Here are some great articles that I recommend reading that will help you learn how to save money and make extra money:

- 30+ Ways To Save Money Each Month

- 15 Reasons You’re Broke And Can’t Save Money

- 12 Work From Home Jobs That Can Earn You $1,000+ Each Month

- 50 Easy Ways To Save Money – Start Saving Thousands Each Year

The power of compound interest.

Saving for retirement as soon as you can is a great thing, especially because of compound interest.

With compound interest, time is on your side- meaning you should start saving money as early as you can.

Compound interest is when your interest is earning interest. This can turn the amount of money you have saved into a much larger amount years later.

This is important to note because $100 today will not be worth $100 in the future if you just let it sit under a mattress or in a checking account. However, if you invest through your retirement account, then you can actually turn your $100 into something more. When you invest, your money is working for you and growing your savings.

For example: If you put $1,000 into a retirement account with an annual 8% return, 40 years later you will have $21,724. If you started with that same $1,000 and put an extra $1,000 in it for the next 40 years at an annual 8% return, that would then turn into $301,505. If you started with $10,000 and put an extra $10,000 in it for the next 40 years at an annual 8% return, that would grow into $3,015,055.

So, if you are wondering “How much money should I save for retirement?” you should also focus on the reasons for saving for retirement now, such as:

- It can help make sure you aren’t working for the rest of your life.

- You can retire sooner rather than later.

- You can lead a good life well after you finish working.

- Compound interest means the earlier you save the more you earn.

- You won’t have to rely on your children or others in order to survive.

As you can see, learning how much money you should save, such as for retirement, is very important.

Side note: I recommend you check out Empower (used to be called Personal Capital) if you are interested in gaining control of your financial situation. Empower is free, and it allows you to aggregate your financial accounts so that you can easily see your whole financial situation, including investments.

So, what’s your answer for when a person asks “How much money should I save?” What are you currently saving for? What percentage of your income do you save?

Leave a Reply