Are you looking to learn how to create family emergency binders? Here’s the in case of emergency binder template along with answers to your question.

Are you looking to learn how to create family emergency binders? Here’s the in case of emergency binder template along with answers to your question.

In our household, I manage most of the bills, financial accounts, and more. I know I’m not alone either – in most families, one person usually handles all of these things.

I’ve been in charge of our important information for years, mainly because it’s just something I know I can do and we’ve fallen into a routine now after doing this for so long.

We have since realized that this could turn into a financial disaster. I manage everything just from my memory, so nothing is actually written down and most of our bills are either auto-pay or paperless, so there is no paper record in our home of anything either.

This could be a disaster because if something were to happen to me, I honestly do not know what Wes (my husband) would do. It would make everything much more difficult for him when he would already be having a hard time, and that is not something anyone wants to deal with. Having some sort of financial emergency plan is something we need to create.

While to some this situation may be no big deal, I know there are many, many families who would be very lost if something were to happen to the person who usually manages their financial situation. Accounts could get lost, passwords would be unknown, bills may be forgotten about, life insurance may be hard to find, and more.

It’s best to keep a family emergency binder of everything just in case something were to happen, even if it’s something no one ever wants to think about. Having one just makes life so much easier.

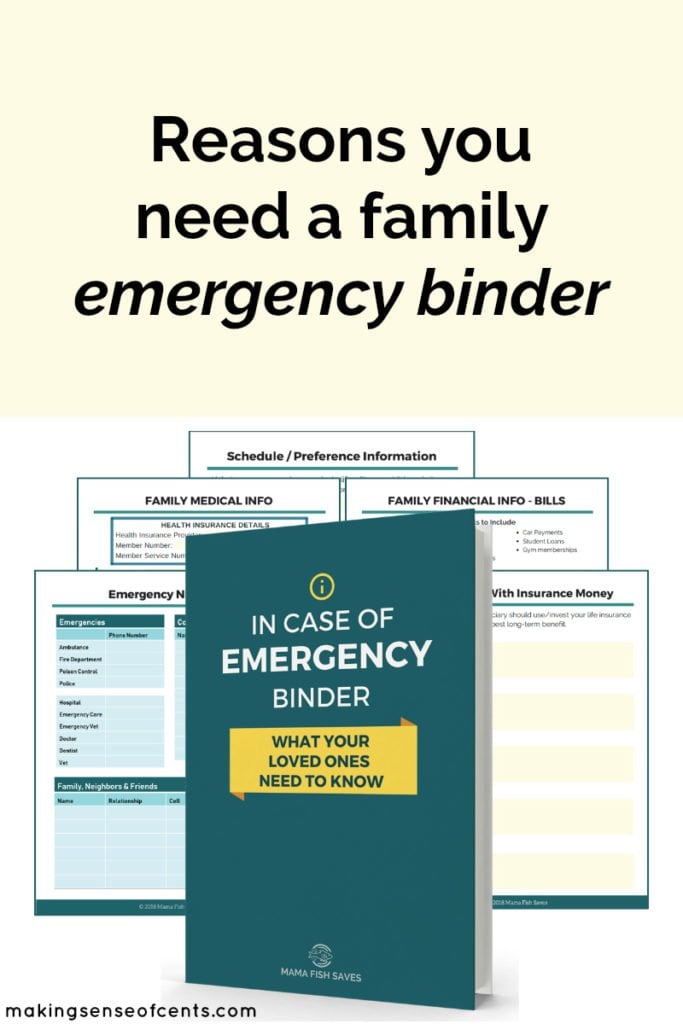

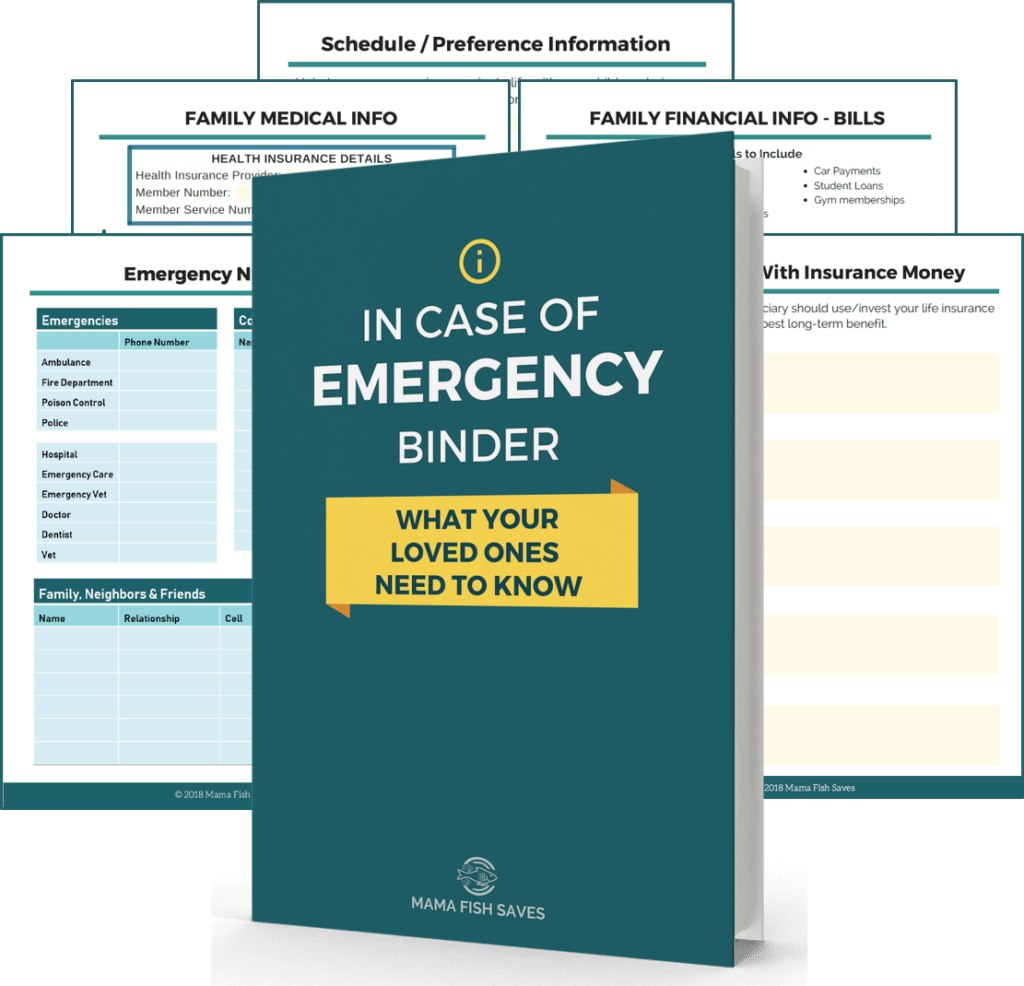

My top tip is to check out the In Case of Emergency Binder to help you with creating your own emergency binder. This is a 100+ page fillable PDF workbook. The In Case of Emergency Binder was created to remove significant complications from the process and help you actually get your important information ready. The research is done, the workbook is put into easy to follow sections, and everything you need is included. Please check it out here.

I asked Chelsea, the creator of the In Case of Emergency Binder to share why having one is so important. Below is her guest post. Enjoy!

Answers to 7 Common Questions About Family Emergency Binders

Hi, all! I’m Chelsea Brennan and I am so grateful to Michelle for having me visit and talk about an topic near and dear to my heart – emergency binders.

Three years ago, I found myself in a basement office with awful fluorescent lighting, five months pregnant, waiting for a nurse to call me back for a life insurance physical. At 25-years-old, I’d never really contemplated my mortality. I was invincible, right?

At the time, I was a hedge fund analyst managing over a billion dollars in assets. I was about to become a first-time mom, and my husband was making the transition to stay-at-home dad. I was over the moon.

It was clear that life insurance was a necessity. I had seen the aftermath of my neighbor’s 31-year-old daughter, a single mother, passing away suddenly without a will or insurance policy. Not pretty. But it wasn’t until I was sitting in that office that I realized my husband would have no clue, zero, zip how to manage a huge life insurance payout. Especially not alongside his grief and need to continue to parent.

You see, I managed all our investments. (Not overly surprising for a personal finance blogger and investment professional.) I paid the bills, organized the budget, and filled out the paperwork for our mortgage and taxes. We have regular conversations about our finances, but that’s high level. Not nearly enough to guide him through doing it himself.

I knew at that moment that I needed something that could hold his hand through the process. Or another family member’s hand if we were both gone. I started to create the In Case of Emergency Binder.

Creating the In Case of Emergency Binder

That day started a long process of creating a complete In Case of Emergency Binder for our family (initially titled, in a fit of dark humor, the “Chelsea Gets Hit By a Bus Binder”).

Creating the binder, I spoke to over 30 experts – doctors, estate attorneys, conservators, military members – on what we might need. We added emotional things from my mom’s advice on what she needed when she lost a parent as a child and my experience writing letters to my dying grandfather. I tweaked and improved until it represented a complete financial and emotional legacy.

Recently, I made our template available to the world. The 100+ page PDF fillable document includes anything one might need in any kind of emergency.

Emergency preparation has become a topic that is near and dear to my heart. I wanted to help other families get prepared without getting overwhelmed by the task.

Today, I wanted to share the top questions I’ve received on creating an In Case of Emergency Binder, and why you should start one today.

I have a will, why do I need an emergency binder? What is an emergency binder?

A will and life insurance policies are pillars of estate planning. But they aren’t the whole picture.

First off, the business of your life goes far beyond what is covered by those puzzle pieces. A will and life insurance policy won’t tell your next-of-kin what bills were on auto-pay, how to contact all your accounts, or what your memorial preferences were. It won’t explain where you had debts.

In fact, there are even sad stories of individuals who knew their spouse or parents had a life insurance policy but didn’t know where to find it. So, they couldn’t file a claim. Or people whose parents had a will, but it still took well over a year to settle the estate because they couldn’t find deeds, mortgage paperwork, or investment account information. Like my friend whose husband had a safety deposit box for their documents, but she never thought to ask which local bank or where the key was kept. When he died suddenly, she spent weeks trying to track it down.

An emergency binder pulls all these crucial details together to save your family time and emotional energy during an already stressful period.

Second, a will and life insurance policy only provide benefit in case of death. But emergencies stretch far beyond this ultimate catastrophe. An emergency binder has what you would need to get a handle on things after a house fire, if one parent became incapacitated, or if someone else needed to step in and care for your pets or kids due to travel delays or medical emergencies and more.

Creating a complete emergency binder fills in the gaps. It paints a full picture, so everything you need in a crisis is at your fingertips.

Do I only need one if I’m married or have kids?

No!

If you’re single and have a medical emergency or pass away, it is even more likely that whoever is left to handle your affairs won’t know where to start. They won’t have watched your day-to-day routine and see where you kept your things. They won’t know where you had investments or which bank services you used. An emergency binder can guide them through.

This is one reason that I recommend people start their emergency binders as soon as they are out of school and get their first jobs. Many people in their early twenties think that if something happened, their parents could step in. But in most states, once you are 18-years-old, your parents are legally strangers to you. Doctors will give them updates on your status, but can’t have a say in your care. Creating an emergency binder, with a durable medical power of attorney, will allow a family member or friend you trust to make important decisions if you weren’t able to make them yourself.

What should I include in an emergency binder? What should be in a family emergency binder?

Putting together our emergency binder took a lot of research. The way it looks today is drastically different than when I first started to compile it three years ago. But here’s the basics of what should be included.

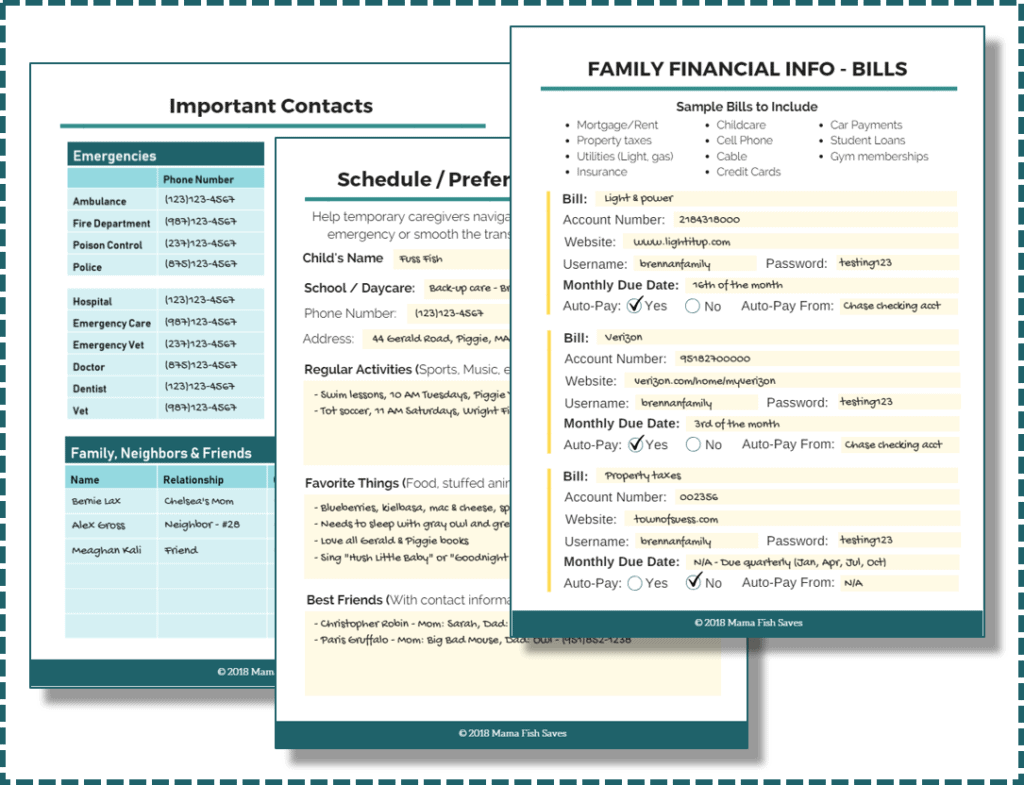

The binder now has two main sections. The Basic Information section covers:

- Household Contact Numbers

- Key Personal Documents: Birth certificates, marriage license, social security cards, copies of passports

- Medical Information

- Childcare & Pet Care Details

- Insurance Documentation & Details

- Basic Financial Information: Properties, regular bills (including what’s on auto-pay), cash accounts, and credit cards

The Need to Know section, which we would only need if one of us died, covers:

- Where to Find Original Documents & Keys

- Employer Information

- Social Media, Email, & Website Logins

- Investment Details (Including a strategy description, trusted professionals to turn to, and what to do with life insurance money)

- Memorial Service Preferences

- Letters to Loved Ones

Writing letters to loved ones was probably the hardest part of compiling this binder for me. But there are things my boys aren’t old enough to hear yet that I would want them to know. And if they had to be raised by someone other than Jeremiah and me, there’s so much I want to say to that person. I also know my mom, who lost her father when she was young, would love to have more notes from him. So, my husband and I did the emotional work to add that information.

Will this only be useful in emergencies?

We have been lucky enough not to have an actual emergency since creating our binder. But we use it all the time.

Wondering where an important document is? It’s in the binder.

Leaving the kids with their grandparents for the weekend? Handoff the household, medical, and caregiver sections of the binder. It has everything they need. (Including medical powers of attorney in case the kids get sick or hurt.)

Just moved? We recently changed states and had to update our address information for all our investments, bank accounts, and recurring subscriptions. I pulled out our binder and logged into every account listed, so I knew that I didn’t miss anything.

The fact is, creating a binder like this organized all your family’s information in one place. It makes finding any piece of information quick and easy. Chances are, you’ll find yourself referring to it often.

How do I keep it updated?

Such an important question. Even a stale binder will be more useful than nothing in an emergency, but for its full benefit, you need to make time to keep it up-to-date.

I recommend setting a notification in your phone to flip through your binder once a year and update any stale information.

However, if you want to keep it constantly up-to-date, you need to build a habit around your emergency binder. Every time a major life event happens in our house – a new asset (like a house or car), new insurance policy, or new doctor – my next thought is that we’ll have to update the ICE binder.

Keeping the binder in the back of my mind means I only have to update one small section at a time, instead of getting overwhelmed by multiple changes every year.

Is it safe to keep all this information in one place?

In a world where identity theft is rampant, pulling together all your most private information in one place seems dangerous. It certainly did to my husband (who can border on a bit paranoid). But with a little careful thought about where we kept our binder, we were able to balance the risk and reward.

Our binder is broken into two sections, and the In Case of Emergency Binder workbook is split up the same way. The ‘Basic Information’ section, which we need more often, stays on a shelf in my office. It has less sensitive information, and in rural Connecticut, there aren’t a lot of people traipsing through there. The ‘Need to Know’ section and our original documents stay locked in a fireproof safe. I also save a digital copy of both binders on a thumb drive that stays locked at my mom’s house. Once a year, I take the jump drive and save an updated file.

We choose not to keep this information online. Deciding to make the PDF workbook fillable was a tough one for me. I didn’t want others to compile this information and save it in a risky place. So, if you purchase the workbook, or choose to make your own file online, please take steps to protect your data.

I recommend LastPass since it encrypts your files and you can safely share with family members or designate a next of kin. But Google Drive and Dropbox are also reasonably secure. Just make sure your password for those services aren’t used for anything else and are more complicated to hack than “Password123”.

Could someone come into our house, break into the safe, and steal our binder? Sure. But the odds seem low enough that I’m willing to take the risk for the comfort it provides my family.

Why should I pay for a workbook like this?

I’ll tell you what. Nothing in the In Case of Emergency Binder is inherently new. You could head to Google, do a bunch of searching, and compile what you need. You can call doctors and talk to your estate attorney to make sure you haven’t missed anything.

But here’s the catch. You probably won’t.

Our lives are so busy that essential things fall to the bottom of the list because there just isn’t time. I created the In Case of Emergency Binder to remove some significant hurdles from the process and ensure that you actually get your crucial information on paper. The research is done, the workbook is broken down into easy to follow sections, and everything you need is included.

Why should you pay for something like this? Because it will save you time and mental energy. And ensure your family has what they need if you ever do face an emergency.

Ready to get started? Create your family’s emergency binder today!

Building our family’s emergency binder wasn’t easy. It required thinking about what could happen and our wishes in those difficult circumstances. But that feeling when it was done?

Total relief.

I know that if I was gone tomorrow, I have done this one hard thing to make it easier for them to carry on without me. And now, you can too.

The In Case of Emergency Binder is a 100+ page fillable PDF workbook to guide you through creating your own emergency binder.

Author Bio: Chelsea Brennan is the founder of Mama Fish Saves, a personal finance blog that focuses on family finance, investing, and reducing money stress. Chelsea is an ex-hedge fund investor whose writing has appeared in a wide array of publications, including Forbes, Business Insider, Haven Life, and more.

Do you have a family emergency binder? Why or why not?

Leave a Reply